ARV is the single most important number in a flip, and the one investors are worst at estimating.

It sets your maximum offer. It sets your loan amount. It sets your profit. Overstate it by 5% and a $50,000 profit becomes $25,000. Overstate it by 10% and the deal loses money.

And there’s a structural problem: you’re estimating the value of a property you badly want to buy. Motivated reasoning does the rest.

What ARV Means

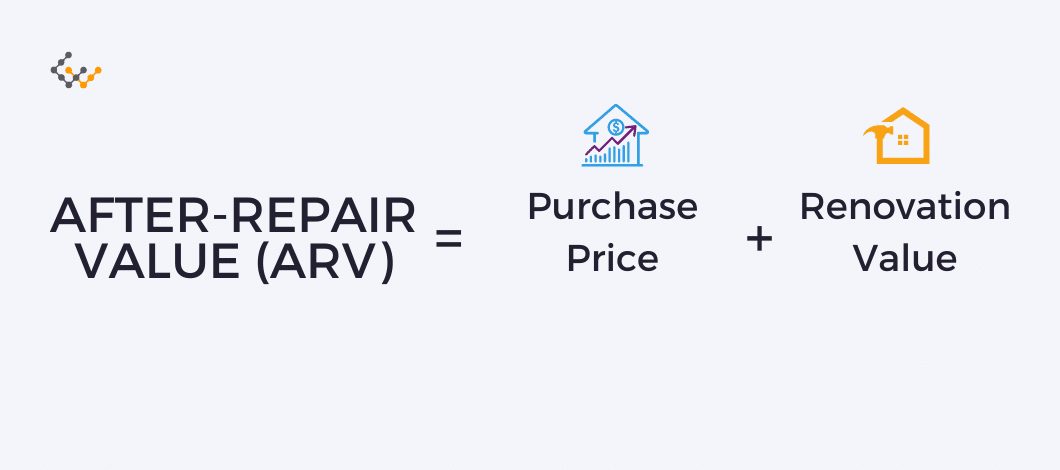

After Repair Value is what the property will sell for once the renovation is complete — not what it’s worth today, and not what you hope it fetches.

It’s the number lenders underwrite against. On a fix and flip loan capped at 90% LTV, the lender is measuring the loan against ARV, which is why an inflated estimate doesn’t just hurt your returns — it can get your loan resized after the appraisal comes back.

The Comparable Sales Method

Appraisers use it. So should you.

Step 1: Find genuine comps

You need recently sold properties — not active listings, not pending, sold. Active listings tell you what sellers hope for. Sold comps tell you what buyers paid.

Comp criteria, in order of importance:

- Sold within 3–6 months. Older sales reflect an older market.

- Within half a mile, and critically, on the same side of any dividing line — a highway, a school district boundary, a railroad.

- Similar square footage, within about 20%.

- Same bed and bath count.

- Similar age and construction.

- Similar condition to your post-rehab property, not its current state.

That last one is the whole game. You’re comparing against renovated homes, because that’s what yours will be.

Step 2: Calculate price per square foot

Three renovated comps near a 1,800 square foot subject property:

| Comp | Size | Sold Price | $/sq ft |

|---|---|---|---|

| A | 1,750 sq ft | $480,000 | $274.29 |

| B | 1,900 sq ft | $515,000 | $271.05 |

| C | 1,820 sq ft | $495,000 | $271.98 |

Average: $272.44 per square foot

Step 3: Apply it to your property

1,800 sq ft × $272.44 = $490,392

Round down. Call it $490,000.

Notice how tight those three comps are — within $3.24 per square foot of each other. That tightness is a signal the estimate is reliable. When your comps range from $240 to $310 per square foot, you don’t have an ARV. You have a guess with a decimal point.

Adjusting Comps

Price per square foot alone is crude. Real appraisers adjust for differences:

- Extra bathroom: add roughly $10,000–$20,000, market dependent

- Garage vs no garage: $10,000–$25,000

- Finished basement: counted at a fraction of above-grade square footage, often 40–60%

- Pool: highly market dependent, and sometimes a negative

- Lot size: matters more in some markets than others

- Backs to a busy road: subtract, meaningfully

If a comp sold for $480,000 but has a two-car garage your property lacks, adjust that comp down before averaging. You’re asking: what would this comp have sold for if it were identical to my property?

The Biases That Wreck ARV

Comp shopping

Pulling twelve comps and using the three highest. Everyone knows this is wrong. Nearly everyone does it anyway, usually without noticing. The tell is when you find yourself explaining why the low comps “aren’t really comparable.”

Counting your own labor as value

Buyers pay for a finished house. They don’t pay a premium because you personally tiled the bathroom.

Overimproving

If every comp on the street sold with laminate counters, quartz won’t lift your sale price by the $8,000 it cost. It might sell the house faster. That’s a real benefit — but it’s a speed benefit, not a price benefit, and it shows up in reduced holding costs, not in ARV.

Assuming appreciation during the hold

You might hold six months. Do not build market appreciation into ARV. If it happens, it’s upside. If you’ve priced it in and the market flattens, your margin is gone.

Trusting automated estimates

Zillow’s Zestimate and similar tools are useful for a first screen and nothing more. They cannot see condition, and condition is the entire premise of a flip.

How to Sanity-Check Your Number

- Pull comps yourself, then have an agent pull them independently. If your ARV is 8% above theirs, yours is wrong.

- Look at days on market for your comps. If renovated homes at your price point sit for 90 days, your holding costs are higher than you modeled.

- Check the ceiling. What’s the highest sale in the neighborhood in the past year? If your ARV is above it, you need an extraordinary reason.

- Run the deal at ARV minus 5%. Does it still work? If a 5% miss turns profit into loss, the margin was never there.

ARV and Your Loan

Lenders order their own appraisal. If it comes in below your estimate, your loan amount shrinks and you cover the difference in cash. This is the moment an inflated ARV becomes a personal financial problem rather than a spreadsheet error.

Conservative ARV protects you twice: it keeps you from overpaying, and it keeps you from being surprised at closing.

Putting It to Work

Once you have a defensible ARV, it drives everything else. The 70% rule uses it to set your maximum offer. Your fix and flip loan is sized against it.

Model the whole deal with our fix and flip calculator, then read what a flip actually costs to make sure you’ve included the lines that disappear from napkin math.

Apply now when you’re ready to see terms.

Adjustment values, price-per-square-foot figures, and comp examples above are illustrative and vary substantially by market. ARV is an estimate, not a guarantee, and lender appraisals govern loan sizing. Nothing here is a commitment to lend or financial, tax, or legal advice. Consult a licensed appraiser or real estate professional for a valuation.